Education is often called an investment in the future, and in many ways that is true. A strong degree, a practical course, or a valuable skill program can open doors that would otherwise stay closed. In 2026, however, the cost of education has become a serious financial challenge for many families. Tuition fees are rising, living expenses in major cities are high, and overseas study can place enormous pressure on household finances. This is why education loans have become an important option. They help students continue their academic journey, but they also create a responsibility that cannot be ignored.

An education loan can be a useful bridge between ambition and affordability. It allows students to pursue higher education without forcing families to liquidate every saving at once. In some cases, it makes quality education possible when it would otherwise remain out of reach. That is the positive side. The difficult side is that many students and parents focus heavily on admission and course selection, but not enough on repayment planning. They treat the loan as a problem for the future. That approach can lead to stress later.

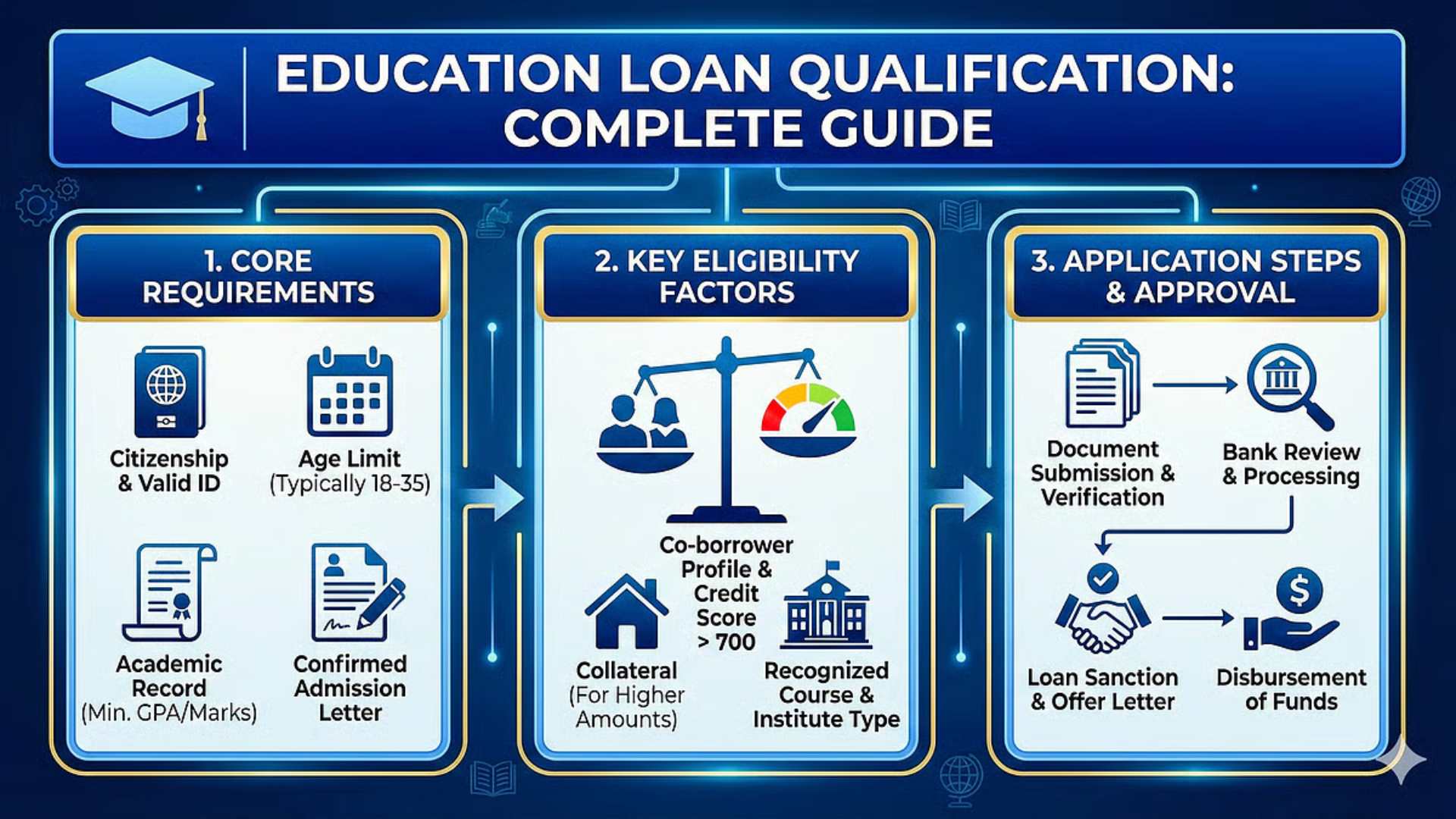

The first thing students and parents must understand is that an education loan is not just about getting funds approved. It is about asking whether the course, college, and future earning potential justify the borrowing. This does not mean education should be judged only in salary terms, but financial reality still matters. A loan for a course with weak employment prospects can become a burden quickly. Passion matters, but so does practical planning.

Before taking a loan, the family should think honestly about the likely return on the education. Will the course improve career prospects in a meaningful way? Is the institution recognized and respected? What are the average placement trends or realistic job paths after graduation? If the student is planning further study immediately after the current program, how will that affect repayment? These are not negative questions. They are responsible questions.

In many households, education decisions are emotional. Parents want to support their child’s dreams. Students want the best possible college or the chance to study in a major city or another country. That emotion is understandable and often beautiful. But when large borrowing is involved, emotion must be balanced with logic. A course should not be selected only because it sounds prestigious. It should also make financial sense for the family’s situation.

Another important point is that education loans often come with a moratorium period. This means repayment may start after the course ends or after a certain time, depending on the lender’s structure. Many students hear this and feel relieved. They assume there is nothing to worry about until graduation. But smart planning begins much earlier. Interest may still accrue, and the total repayment burden may grow during the study period. Families should understand exactly what happens to interest before full EMI repayment begins.

One powerful habit is to estimate future EMI at the time of borrowing, not after the course is completed. Students and parents should ask: once repayment starts, what will the likely monthly obligation be? If the initial salary after graduation is modest, can that EMI still be handled? If not, what is the backup plan? Will parents support repayment for a while? Can partial interest payments be made during the course to reduce pressure later? Planning early creates control.

In 2026, education loan amounts can vary widely depending on the course, country, institution, and collateral structure. Domestic study may require smaller borrowing than international education, but even local higher education can create a significant debt load for middle-income households. This is why students must learn to separate educational value from lifestyle cost. The loan should fund learning, not unnecessary spending. Living within a reasonable student budget can make a big difference to the final burden.

For example, a student going abroad may feel tempted to spend more on accommodation, lifestyle, gadgets, travel, and social experiences because the loan money is available. But borrowed funds are not free money. Every extra expense may eventually return as repayment pressure. Students who understand this early usually handle their loan journey much better. Financial awareness during study years is one of the strongest forms of maturity.

Parents also need clarity about their own role. In some families, the student is expected to repay everything after graduation. In others, parents intend to share the burden. Problems arise when these expectations are never discussed clearly. A student may believe the family will help for the first few years, while parents quietly assume the student will become fully independent immediately after getting a job. Honest conversation prevents confusion and resentment later.

Credit discipline matters in education loans just as it does in any other loan. If parents are co-borrowers, their financial profile matters. If collateral is involved, the risk becomes more serious. The loan should be taken with full awareness of the obligation. This is not just about getting admission. It is about protecting the family’s financial stability while supporting the student’s future.

Course selection plays a huge role in repayment comfort. Programs linked to strong employability often make loan repayment easier because salary entry points are better. Courses with longer job uncertainty require more caution. This does not mean students should only choose high-paying fields. It means they must align aspirations with reality. If the course is more uncertain in financial terms, then the loan amount should ideally be kept lower, or the family should prepare stronger backup support.

Students should also think beyond the degree itself. Internships, skill development, networking, communication ability, and practical readiness can influence how quickly a graduate begins earning. A degree alone is not always enough anymore. In a competitive job market, students who use their study years well often enter repayment with more confidence because they are better prepared for work.

Another wise strategy is making small payments whenever possible. If parents can pay at least part of the interest during the study period, the overall burden may reduce. If the student earns through internships, freelance work, assistantships, or part-time opportunities, even small contributions can create a healthier loan structure. These efforts may not eliminate the debt, but they build financial discipline and reduce future pressure.

There is also the emotional side of education loans. Many students carry silent stress about becoming a burden on their family. Many parents quietly worry about how repayment will work if the child does not get a job quickly. These feelings are normal, but they become heavier when there is no plan. A loan becomes less frightening when everyone understands the path ahead.

Families should also be cautious about borrowing more than necessary just because it is available. It may feel safer to have a larger sanctioned amount, but unnecessary borrowing increases future repayment. A disciplined budget during the education period can reduce long-term strain. Borrow what supports the academic goal, not what supports comfort without purpose.

Lenders, documents, and approval conditions may differ, but one principle remains constant. The best education loan is not the biggest one. It is the one that helps the student move forward without creating unmanageable stress later. Families should compare terms carefully, understand repayment clauses, and avoid signing anything they do not fully understand.

There is also a difference between investing in education and outsourcing financial planning to hope. Hope is important, but it should not replace preparation. Students may believe they will get a great salary immediately after graduation. Sometimes that happens. Sometimes it does not. The job market can shift. Visa issues, industry slowdowns, health problems, relocation challenges, or career changes can affect the timeline. That is why loan planning must include uncertainty, not just best-case scenarios.

For students, an education loan can also be a lesson in adulthood. It teaches responsibility, delayed gratification, budgeting, and long-term thinking. These lessons matter beyond repayment. Students who understand money early often make stronger decisions in career and life later on.

In 2026, education remains one of the most valuable things a person can pursue, but the financing of that education must be handled wisely. A loan should support a future, not overshadow it. Students and parents must think together, question carefully, compare realistically, and plan repayment long before the first EMI arrives.

An education loan can absolutely be worth it. It can create opportunity, mobility, and confidence. But its success depends on preparation. Choose the course thoughtfully. Borrow responsibly. Keep the budget practical. Understand the full cost. Plan for the EMI early. And most importantly, treat repayment as part of the education journey, not as a surprise waiting at the end. That is how educational ambition and financial discipline can move together in the right direction.